Can Debt Recycling Help You Pay Off Your Mortgage Faster?

Debt recycling helps Australians pay off their mortgage faster by converting non‑deductible home loan debt into tax‑deductible investment debt. Using equity, strategic investing, and cash‑flow recycling, homeowners can reduce their mortgage term while building long‑term wealth.

Table of Contents

- Introduction: Making Your Home Loan Work for You

- What is a Debt Recycling Strategy?

- How Does Debt Recycling Work? (The 5-Step Cycle)

- Three “Boosters” to Pay Off Your Mortgage Faster

- Case Study: The NetGrowth Approach in Action

- Is Debt Recycling Right for You?

For many Australian homeowners, the mortgage is the single largest financial burden. While making regular repayments eventually leads to ownership, the "traditional" path can take 25 to 30 years and cost hundreds of thousands of dollars in non-deductible interest.

But what if your home loan could actually work for you? Enter debt recycling, a sophisticated yet increasingly popular financial strategy designed to help Australians pay off their home loans years earlier while simultaneously building a wealth-generating investment portfolio.

What is a Debt Recycling Strategy?

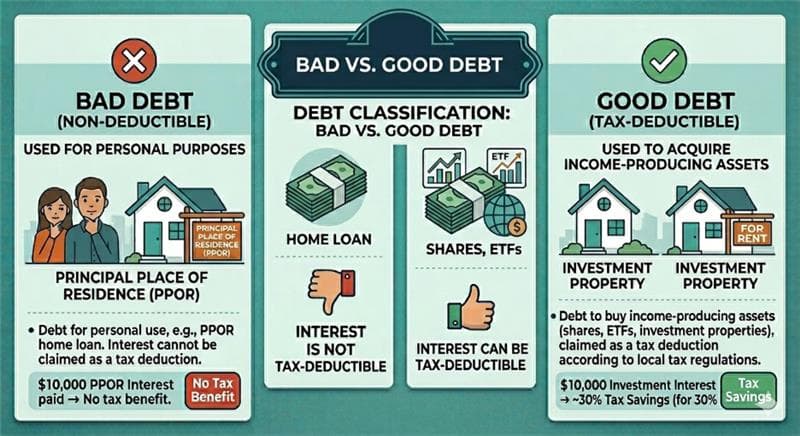

At its core, a debt recycling strategy is the process of replacing "bad debt" with "good debt."

The goal of debt recycling is to progressively convert your non-deductible mortgage into a tax-deductible investment loan without necessarily increasing your total debt level.

How Does Debt Recycling Work?

Step 1: Build Equity

You start by making extra repayments into your home loan or accumulating cash in an offset account. This creates "equity" or available credit.

Step 2: Split and Redraw

Instead of just redrawing the money for a holiday or a new car, you request your bank to create a separate "investment split." You then redraw the funds from this specific split. This is a critical step; keeping the funds separate ensures the ATO can clearly see that the borrowed money is used for investing, preserving its tax-deductible status.

Step 3: Invest in Income-Producing Assets

The redrawn funds are invested into assets that generate assessable income, such as Australian shares with franked dividends, managed funds, or an investment property.

Step 4: Use Income to Smash the Mortgage

This is where the magic happens. Any dividends, rental income, and—most importantly—the tax savings gained from the interest deductions are funneled back into the original non-deductible home loan.

Step 5: Repeat the Cycle

As the non-deductible loan balance drops, you repeat the process: increase the investment split, redraw, invest more, and use the higher returns to pay down the home loan even faster.

How Does Debt Recycling Help You to Pay Off Your Mortgage Faster?

The speed of this strategy comes from three distinct "boosters" that traditional repayments don't offer:

1. Tax Refunds: By claiming the interest on your investment loan as a deduction, you reduce your taxable income. The resulting tax refund is "new money" you can inject directly into your mortgage.

2. Compounding Investment Income: Instead of waiting until your house is paid off to start investing (which could take 20 years), you start immediately. The dividends or rent you receive provide a secondary income stream dedicated solely to debt reduction.

3. The Snowball Effect: As your investment portfolio grows, so does the income it produces. This creates an accelerating cycle where each year you have more "extra" cash to put toward your home loan than the year before.

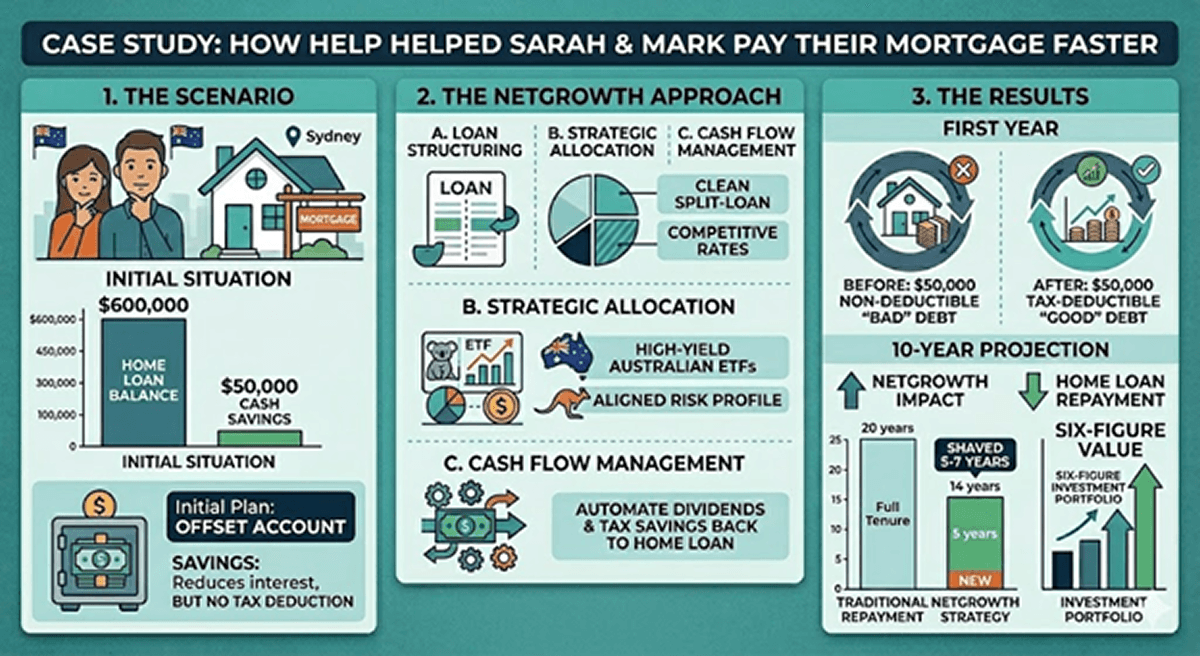

The Scenario:

Sarah and Mark, a Sydney couple came to NetGrowth with a $600,000 mortgage and $50,000 in savings. Left to their own devices, they were thinking to put that $50,000 in an offset account. While this saves interest, it doesn’t grow their wealth or provide a tax deduction.

The Netgrowth Approach:

We advised Sarah and Mark to restructure their finances. We assisted in:

- Loan Structuring: Helping them set up a clean split-loan facility with a competitive interest rate.

- Strategic Allocation: Recommending a diversified portfolio of high-yield Australian ETFs that align with their risk profile.

- Cash Flow Management: Automating the flow of dividends and tax savings back into the non-deductible debt.

The Result: By working with Netgrowth, Sarah and Mark didn't just save interest; they converted $50,000 of "bad debt" into "good debt" in the first year. Over a 10-year period, the combination of tax savings and reinvested dividends could potentially shave 5–7 years off their mortgage and leave them with a six-figure investment portfolio—something they wouldn't have had if they simply focused on "paying off the house" the old-fashioned way.

Is Debt Recycling Right for You?

While powerful, debt recycling is not without risk. It involves leverage, meaning that if your investments decrease in value, you still owe the full amount to the bank. It is best suited for Australians who:

- Have stable, reliable income.

- Hold significant equity in their home (usually 20% or more).

- Are in a higher tax bracket (where the deductions are most valuable).

- Have a long-term investment horizon (7-10+ years).