Reduce Aged Care Costs in Australia with Smarter Financial Planning

Reducing aged care costs in Australia requires smart financial planning around accommodation payments, assets, and Age Pension entitlements. By understanding RAD and DAP options, managing the family home correctly, and avoiding common mistakes, families can significantly lower fees while securing long‑term care affordability.

Table of Contents

- Introduction: Why Aged Care Cost Planning Matters

- Ensure Aged Care Fees Can Be Covered for Life

- Should You Sell or Keep the Family Home?

- Choosing the Right Accommodation Payment Option

a. Refundable Accommodation Deposit (RAD)

b. Daily Accommodation Payment (DAP)

c. Combination Payment Options

- Strategies to Reduce Means-Tested Care Fees

- How to Increase Age Pension Entitlements in Aged Care

- Common Financial Mistakes Families Make

- Case Study: How Netgrowth Helped a Client Reduce Aged Care Costs

- The Value of Professional Advice

Reducing aged care costs in Australia requires smart financial planning around accommodation payments, assets, and Age Pension entitlements. By understanding RAD and DAP options, managing the family home correctly, and avoiding common mistakes, families can significantly lower fees while securing long‑term care affordability.

Moving a loved one into aged care can be both an emotional and financial challenge for many Australian families. Between accommodation costs, daily care fees, and means-tested charges, the financial side of aged care can feel overwhelming. However, with careful planning and a good understanding of the system, there are several strategies that can significantly reduce aged care costs while ensuring your loved one receives the care they need.

Australia's aged care system is designed to ensure that people can access care regardless of their financial situation, with government subsidies helping cover a significant portion of costs. However, residents are still required to contribute through accommodation payments and ongoing care fees, which can vary depending on income, assets, and personal circumstances. By understanding how the system works and implementing smart financial strategies, families can manage aged care costs more effectively and reduce unnecessary expenses.

Below are some of the most effective strategies to reduce aged care costs in Australia.

The most important step in aged care financial planning is ensuring that fees can be covered for the remainder of a resident's life. Aged care costs can change over time due to adjustments in government policies, income levels, and personal circumstances. Planning ahead helps families avoid financial stress later.

Start by calculating all expected income sources such as:

- Age Pension

- Superannuation pensions

- Rental income

- Investment dividends

- Overseas pensions or other income streams

Then estimate the ongoing aged care expenses, including the basic daily fee, accommodation payments, and potential means-tested care fees. If there is a gap between income and expenses, savings or other assets may need to be used to cover the shortfall.

Financial modelling can help families project costs over several years to ensure funds last throughout the resident's stay in care. Proper planning can prevent situations where assets run out prematurely.

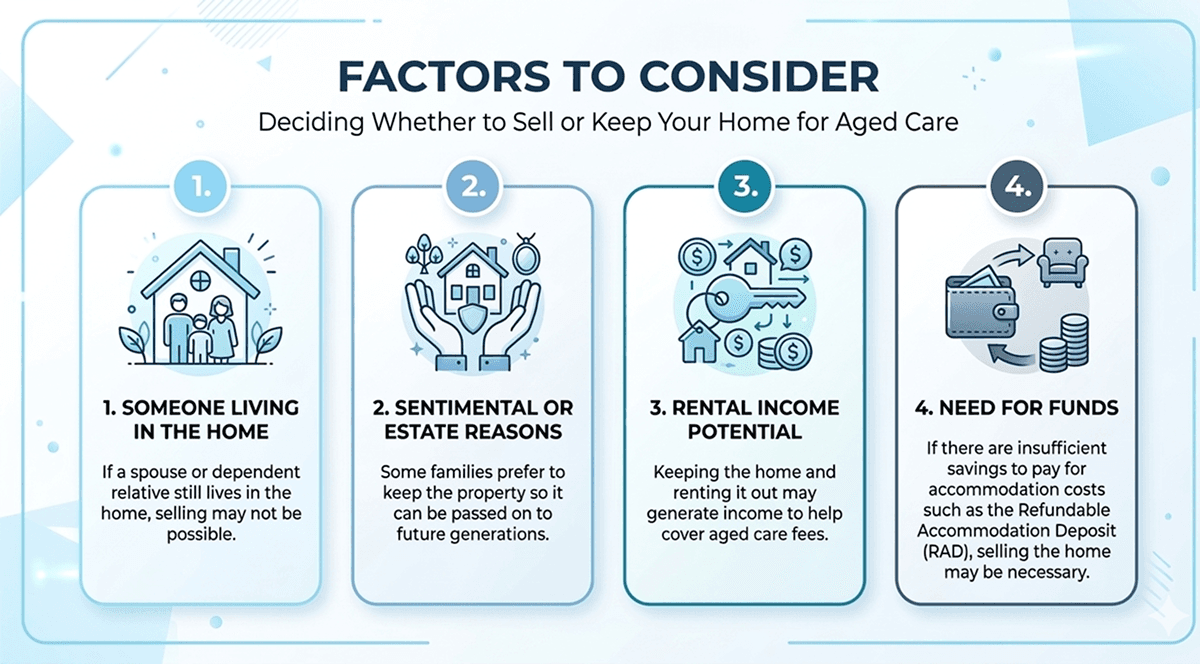

One of the biggest financial decisions families face is whether to sell the family home when someone enters aged care.

There is no single correct answer, as the best option depends on several factors.

How the Home Is Assessed

For pension purposes, the home can remain exempt for the first two years after entering aged care. However, after that period it may be treated as an investment asset, which can affect pension eligibility.

For aged care means-testing, the home is assessed but its value is capped at just over $200,000. This means selling the property and holding the full proceeds may increase assessable assets and lead to higher care fees.

Because of these complexities, families should carefully assess whether selling or retaining the home will produce the best financial outcome.

Accommodation payments are one of the largest costs in residential aged care. These payments typically come in three forms:

Refundable Accommodation Deposit (RAD)

This is a lump sum payment for accommodation. The full amount is usually refunded when the resident leaves the facility, although future reforms may allow providers to retain a small percentage annually.

Daily Accommodation Payment (DAP)

Instead of paying a lump sum, families can pay a daily fee similar to rent. The rate is calculated using the government-regulated Maximum Permissible Interest Rate.

Combination Payment Options

Many families choose a combination of RAD and DAP, paying part of the accommodation cost upfront and covering the remainder with daily payments.

Selecting the right structure can significantly affect overall financial outcomes. For example, paying more toward the RAD may reduce ongoing daily accommodation costs and can also improve Age Pension eligibility because RAD payments are exempt from pension asset testing.

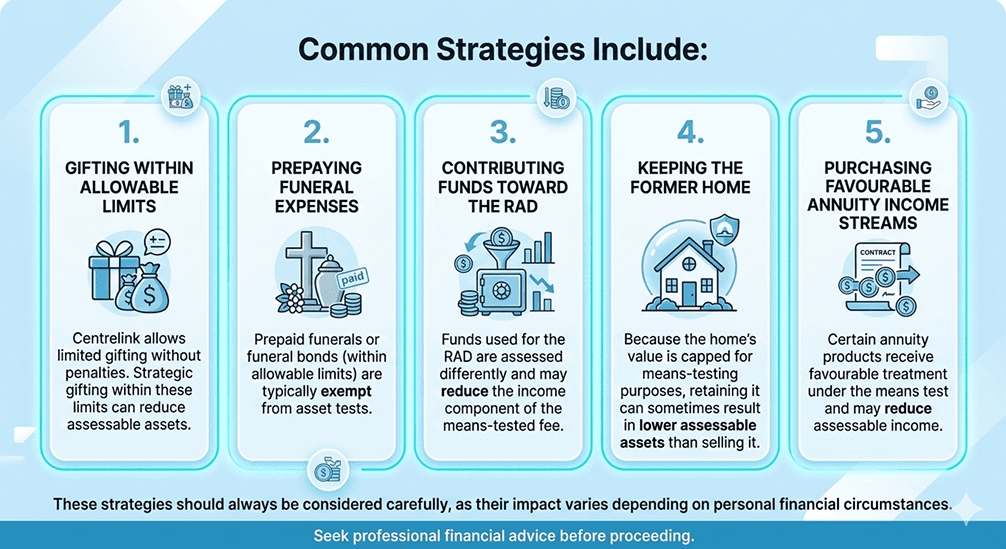

The means-tested care fee is determined by a resident's income and assets. While the government subsidises a large portion of care costs, residents who have greater financial resources are expected to contribute more.

However, there are legitimate strategies that may reduce this fee.

Another effective strategy for managing aged care costs is maximising Age Pension payments. The pension often forms a major source of income used to cover care expenses.

Several financial strategies that reduce means-tested care fees can also increase pension entitlements.

For example:

- Paying a RAD may reduce assessable assets for pension calculations

- Gifting within limits can lower asset levels

- Prepaid funeral arrangements can remove assets from assessment

- Retaining the family home can preserve pension eligibility for a period

When a member of a couple enters care, they may also be classified as a "couple separated by illness." This classification can sometimes increase the pension payments received by the couple overall.

Properly structuring income and assets can therefore lead to higher pension payments and lower aged care costs.

Many families unintentionally make costly financial mistakes when arranging aged care.

Some of the most common include:

Contributing Too Much to the RAD

While paying a large RAD can reduce daily payments, contributing too much may leave insufficient cash to cover ongoing expenses.

Paying Too Little Toward the RAD

Conversely, contributing too little may result in high Daily Accommodation Payments that exceed potential investment earnings.

Family Members Funding Costs Incorrectly

If family members loan money to help pay for the RAD, the loan may be treated as an asset of the resident, increasing means-tested fees.

Excessive Gifting

Some families try to reduce assessable assets by gifting large sums to relatives. However, Centrelink continues to assess excess gifts for several years, which can result in higher fees while reducing available funds.

Creating Complex Financial Structures

Complicated financial arrangements intended to hide assets can backfire if Centrelink continues to assess those assets anyway.

Avoiding these mistakes can save families significant money over time.

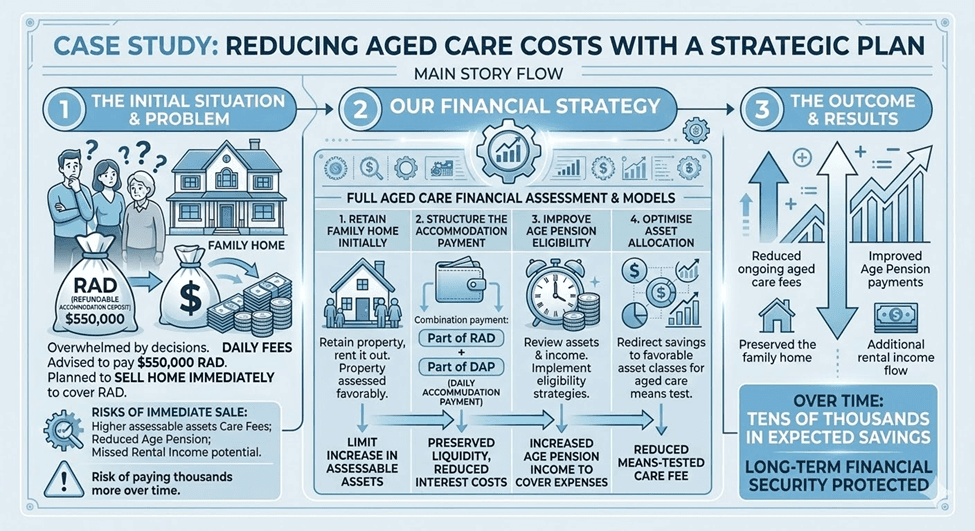

At Netgrowth we regularly assist families who feel overwhelmed by the financial decisions involved in moving a loved one into aged care.

Client Overview

A retired couple owned their family home and had accumulated approximately $550,000 in savings (RAD – Refundable Accommodation Deposit). As they began planning for aged care, they felt overwhelmed by complex decisions and rising daily care fees.

The Initial Situation & Problem

- Pay a $550,000 RAD

- Planned to sell their family home immediately to cover costs

Challenges Identified

- Emotional stress around selling the family home

- Lack of clarity on the most cost-effective strategy

- Risk of making rushed financial decisions

Risks of Immediate Sale

- Increased means-tested care fees due to higher assessable assets

- Loss of potential rental income

- Reduced age pension entitlements

- Paying thousands more over time in aged care costs

Our Financial Strategy

We implemented a comprehensive aged care financial assessment and modelling approach, focusing on optimising both cash flow and long-term outcomes.

Key Strategies

Retain the Family Home

- Kept the property instead of selling

- Generated rental income

- Reduced impact on assessable assets

Restructure Accommodation Payments

- Split payments into:

- Part RAD (lump sum)

- Part DAP (Daily Accommodation Payment)

- Improved cash flow flexibility

Improve Pension Eligibility

- Reviewed all assets and income

- Applied strategies to maximise Age Pension entitlements

Optimise Asset Allocation

- Redirected savings into more favourable asset classes

- Reduced exposure to means testing

The Outcome & Results

Financial Benefits

- Reduced ongoing aged care fees

- Improved Age Pension payments

- Created additional rental income stream

Lifestyle & Emotional Benefits

- Preserved the family home

- Reduced financial stress and uncertainty

- Maintained greater control over financial decisions

Long-Term Impact

- Achieved tens of thousands of dollars in savings over time

- Strengthened long-term financial security

This case study highlights an important lesson: aged care financial decisions should never be made without proper advice.

Many families assume they must sell the family home or pay the full RAD immediately. However, as this example shows, the right financial strategy can significantly reduce costs and improve outcomes.

At Netgrowth , we specialise in helping families navigate the complex aged care system. Our advisers provide personalised financial modelling and strategic advice to ensure your loved one's care is both financially sustainable and aligned with your family's goals.

If you or a family member are considering aged care, speaking with an experienced financial adviser early can make a substantial difference to the financial outcome. Contact us today to get personalised Aged Care Advice.